Every day, legitimate customers reach checkout and attempt to complete a purchase. They have available funds. Their card is active. They want to buy.

Yet the transaction gets declined.

The customer leaves. The sale disappears.

While most merchants spend thousands of dollars on attracting new customers, a big part of your revenue is hidden in false declines that can and should be recovered.

In this article, we’ll talk about what false declines are in eCommerce, why they occur, and how your declined payments can be be recovered with AI.

What’s a False Decline?

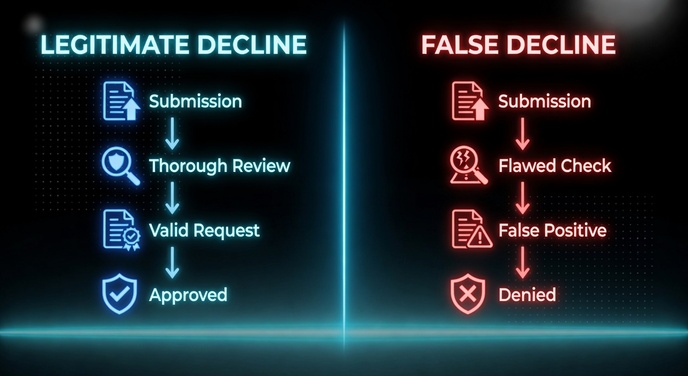

To get a better understanding of a false decline, let’s take a look at a declined payment first.

A declined payment (or a declined transaction) is a legitimate decline, where a legitimate transaction fails for a reason. Examples include:

- Insufficient funds

- Lost or stolen cards

- Expired cards

- Invalid card details

In these situations, the transaction genuinely cannot be completed.

A false decline occurs when a legitimate transaction is rejected despite the customer being fully capable of completing the purchase.

The customer:

- Has sufficient funds

- Owns the card

- Entered correct information

- Intends to purchase

Yet the payment still fails.

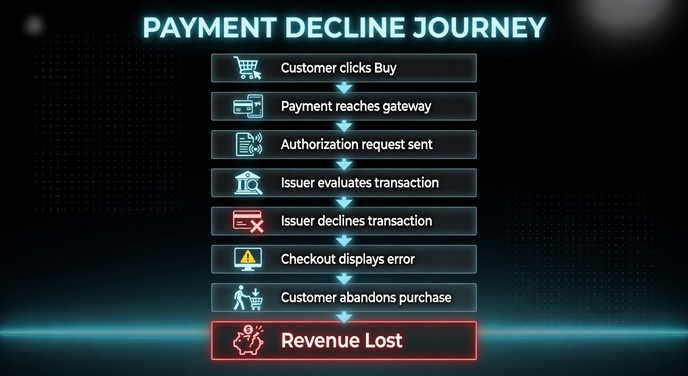

Behind the scenes, the process typically looks like this:

Traditional payment stacks stop here.

Here's the interesting thing: if everything is okay with your customer and their money, why do false declines happen?

Why False Declines Are Exploding in eCommerce

The reasons why false declines are killing your revenue might be different. We will focus on the most common and most painful ones.

First of all, with the development of digital payments, security in fintech and eCommerce has become more aggressive. Today’s online shoppers buy from multiple countries, use mobile wallets, subscribe to recurring products, and more. Banks are under pressure to reduce fraud at all costs, and in many cases, any unusual activity from legitimate customers looks suspicious to the systems.

To protect themselves, banks increasingly rely on:

- Automated risk scoring

- Velocity monitoring

- Device fingerprinting

- Behavioral analysis

- Cross-border risk controls

- AI-driven fraud systems

While these systems stop fraud, they also create false positives.

Next, the old good payment stack fragmentation. A single transaction can pass through multiple layers before approval: different gateways, payment processors, MIDs, fraud vendors, routing systems, and even more.

And the truth is that the more layers involved in a transaction, the more failure points occur.

The next logical question is: how do false declines affect your business?

The Real Cost of False Declines

Imagine this: your customer already saw the ad, clicked it, visited your website, added products to the cart, started checkout, and the transaction fails.

The entire acquisition cost is effectively wasted.

To understand the true impact of false declines, let’s take a look at the numbers. For a merchant processing $1M per month, a 10% decline rate can translate into $100,000 in lost revenue. At $10M and $50M in monthly volume, that figure grows to $1M and $5M, respectively.

Even recovering just 20% of those false declines can generate an additional $20,000, $200,000, or $1M in monthly revenue.

How to Recover Failed Payments with AI

Traditionally, to recover a declined payment, you can manually retry transactions or ask customers to try another payment method.

Will that work? It might.

Will it influence your brand’s reputation and trust level? For sure.

AI-powered recovery systems work differently. Instead of treating a decline as the end of the transaction, they analyze why the payment failed and look for the highest-probability path to approval.

1. Processor/Acquirer Switching

We all know firsthand that a payment may fail with one processor but succeed with another. Modern AI-powered recovery infrastructure can do it for you by rerouting declined payments through alternative acquirers, different MIDs, or alternative payment rails.

For example, a Visa transaction declined by one acquiring bank may succeed instantly when AI routes it through another bank with different approval logic.

2. Smart Retry Timing

The good thing is that, in reality, many transaction declines are temporary. This means that the system needs a cooldown period, after which a transaction could be successful.

Thus, instead of automatically retrying immediately, AI systems wait for issuer cooldowns, optimize retry timing, and retry only when the approval probability increases.

To illustrate, a payment declined at 2:01 PM by the system might process successfully a few minutes later, once the issuer's throttling resets.

3. Checkout Recovery Flows

Traditionally, when a payment gets declined, the checkout system simply shows an error message and ends the session.

Modern checkout systems act differently.

Within seconds, when a transaction fails, the checkout system can automatically suggest another payment method like Apple Pay or Google Pay, allow the customer to switch cards instantly, or even continue the checkout flow without forcing the customer to restart the session.

4. AI-Based Authorization Optimization

When applied, modern AI recovery systems analyze a number of payment signals to automatically recover a failed payment:

- BIN data

- Geography

- Device signals

- Historical issuer behavior

- Approval trends

Based on this information, the AI adjusts routing, retry logic, and approval strategies in real time.

For example, the system may learn that a specific issuing bank approves transactions more successfully and automatically optimize for that behavior.

5. Subscription Recovery & Dunning Optimization

Unlike one-time purchases, subscription models depend on successful recurring billing. A single failed payment can kill the entire customer lifecycle. This is where dunning optimization comes into play.

Modern recovery infrastructure optimizes:

- Retry frequency

- Retry timing

- Alternative payment methods

- Customer communication flows

For example, if a subscription payment fails before payday, the AI system may wait until the customer’s payday, retrying just on that day and, this way, dramatically increasing approval probability.

Final Thoughts

In many cases, your customer’s failed payment is a false decline, a sheep covered in a wolf’s skin. Instead of treating it as the end of the customer journey, we suggest considering it a revenue optimization opportunity.

At the end of the day, the easiest revenue growth opportunity is not more traffic, but recovering the payments you have already earned. Merchants that actively optimize payment recovery with AI will be better positioned to improve customer experience and eventually protect revenue.